Purpose and scope

This document provides guidance for NIHR Global Health Research Programme contract holders financed via Official Development Assistance (ODA) funds on how to deal with foreign currency denominated transactions, that is any currency other than the contract currency, GBP (UK Sterling, £).

Terminology

In this guidance, different exchange rate terms are used and their meaning are as described below.

- Contract currency is the currency stated in the contract and the project costing/budget. Contract currency, also referred to as the reporting currency, is the currency used in financial reports submitted to the funder. For the purpose of this guidance, contract currency is the preferred term.

- Functional currency is the currency of the primary economic environment in which the entity operates. The primary economic environment in which an entity operates is normally the one in which it primarily generates and expends cash (Page 1, International Accounting Standard 21). For example, some countries use USD as the functional currency.

- Local currency is a currency that can be spent in a particular geographical locality at partner organisations

- Foreign currency is any currency other than the contract currency. All foreign currencies are converted into contract currency using the recommended exchange rates stated in this guidance

Flow of funds

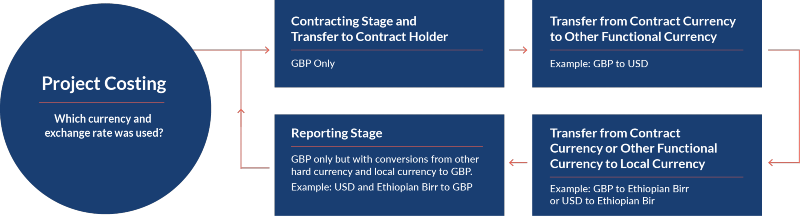

The diagram below shows the flow of funds and the corresponding change in currency from the funder (Department of Health and Social Care, DHSC) to contract holder and subsequently from contract holder to downstream partners.

During project costing, a particular currency and exchange rate will have been used. GBP is used by the funder during the contracting stage and transfer of funds to the contract holder. These funds may then be transferred from contract currency to another functional currency (e.g. from GBP to US dollars, USD). Use of foreign currency continues in conversion of funds from contract currency or functional currency into local currency (e.g. GBP or USD to Ethiopian Birr). Reporting to funder uses GBP only, but with conversions from other hard currency or local currency to GPB (e.g. USD or Ethiopian Birr to GBP).

UK Accounting Practice: International Accounting Standard (IAS) 21

Organisations implementing ODA projects follow International Accounting Standard (ISA) 21, which states: “A foreign currency transaction shall be recorded, on initial recognition in the functional currency, by applying to the foreign currency amount the spot exchange rate between the functional currency and the foreign currency at the date of the transaction”.

Using spot rates, which is usually determined by the financial markets, can bring challenges such as delays in ascertaining daily spot rates or may require additional resources in some contexts such as where ODA projects is implemented. In practice, organisations tend to use average rates for a week or a month, which can be determined in advance. For example, the average exchange rate for the month of January is taken as the rate for February and the average exchange rate for the month of February is taken as the rate for March, and so on.

Good practice exchange rate principles

Good practice principles must meet the following:

- the methodology used to convert foreign denominated transactions must be:

- written down as a policy

- used throughout the project funded i.e. consistently applied

- the exchange rate used must be:

- verifiable through documentary evidence

- real and credible, as determined by the markets. Commonly used sources are Oanda, the Financial Times, XE, etc.

International development organisations working on large contracts in Euros tend to use monthly inforeuro rates.

How exchange rate fluctuations happen

Project costings are usually prepared using exchange rates applicable at the time and period that the project proposal was produced. Contracting tends to happen several months after the proposal submission and the resulting time lag means that exchange rates may have changed favourably or unfavourably.

At contracting, the exchange rates may have moved either favourably or unfavourably against the project costing and organisations are encouraged to discuss if there are significant variations that could affect project delivery, that is, the significant variation is so substantial that the estimated project costs no longer reflects the true cost of the work to be undertaken.

Contract holders normally receive funds in the same currency as stipulated in the submitted costed proposals and contract and therefore there is no exchange rate at this stage. Upon receipt of funds in GBP, the contract holder based in the UK transfers GBP to downstream partners according to agreed functional currency. If the functional currency is the same as contracting currency (GBP), then no exchange variation occurs; but if the functional currency is different, such as USD, then exchange fluctuations are likely to happen. In all countries of operations, local currency is used and spending is in either functional currency or local currency (and in some instances there can be several local currencies).

The flow of funds from contract currency is as follows:

- Contract currency (GBP) - functional currency - local currency

Reporting to the NIHR is in GBP and financial reports are prepared using financial transactions recorded in GBP (receipt of funds), functional currency or local currency. Reporting therefore takes the transactions-to-reporting flow as follows (with foreign currency converted accordingly to GBP):

- Local currency - functional currency - contract currency (GBP)

Exchange rate methodologies to use

For reporting back to NIHR

- Lump sum transfers: UK based contract holders usually prefer to make lump sum transfers or disbursements from UK in GBP to a bank account in the implementing country, which can be in GBP, functional currency such as USD or local currency. Contract holders may choose the exchange rate applied at the point of transfer (disbursement) as the exchange rate to use in reporting. Where an organisation makes periodic transfers, the rates are applied in the reporting either first in first out (FIFO) or on average rate basis, if there was more than one transfer in the reporting period. Reporting must include a schedule of exchange rates used. Using exchange rate achieved at disbursement/transfers has a low chance of unfavourable exchange rates because it uses actual exchange rate achieved.

- Other methodologies for calculating exchange rate to use in financial reporting to the funder that differs from (a) above may be acceptable but need prior agreement with NIHR. Where other methodologies are accepted, NIHR would expect this to be supported by verifiable ‘schedule of exchange rates’.

In business operations

NIHR acknowledges that business operations occur daily and exchange rate used (whether daily or average) need to follow the good practice mentioned in 4.0 i.e. written down as a policy, used throughout project life, verifiable through documentary evidence and real/credible (market driven). If there is more than one NIHR contract held by an organisation where exchange rates are used, we would expect the same policy to be applied across all contracts.

No other methodology will be acceptable apart from 6.0 (I) (a) or (b) above for financial reporting to NIHR and both scenarios will require verifiable ‘schedule of exchange rates’.

Impact of exchange rate movements: exchange gains and losses

Exchange rate movements can result in either exchange gains or exchange losses, which in turn affect project budget costs either positively (gain) or negatively (loss), and impact on the delivery of a balanced budget. The contract holder must monitor exchange movements throughout the lifetime of the project.

Sometimes it is possible that exchange gains and losses will cancel out over time but this does not necessarily result in no impact on project implementation as the currency variations may not happen during the same period with similar project activities.

Exchange gains or losses are borne by the contract holder. This requires the contract holder to exercise prudence in its exchange rate regime. It is the responsibility of the contract holder to report to the assigned Senior Programme Manager (SPM)/Programme Manager (PM), initially via email, whenever either of these situations is likely to occur.

Common ways of dealing with exchange gains and losses

Exchange losses that triggers funding shortfall

If there is a long lapse of time between proposal’s submissions and contracting, resulting in unfavourable exchange rates, provided it is verifiable, the contract holder may request virements between cost categories. The virement request moves funding between cost categories/headings but neither increases the approved costing nor grants additional time. After contracting and during project implementation, contract holders can request:

- Project costing/budget realignment approval to allow movement of funding between cost categories/headings (virements) where this can remedy funding shortfall triggered by currency fluctuations.

- As a last resort and with no guarantee of approval, a variation to contract (VTC) requesting additional funds may be made where the above does not fully resolve the funding shortfall, provided it is fully justified. Since this option is never guaranteed to be approved, it is prudent to make the request on time to allow sufficient time for other alternative solutions to be implemented such as scaling down the level of activities to cover shortfall in funding arising from unfavourable exchange movements.

Exchange gains that triggers results in additional funds

It is always a possibility that exchange gains far outweigh exchange losses i.e. validated and irreversible exchange gains.

Where exchange rate variations cause underspend against the contract value, there are two consequences:

- Unspent funds, which is not encouraged as it can result in undesirable outcomes

- Completion of additional activities so as to spend the physical or liquid exchange gains

The Contract holder must request permission from NIHR to utilise - validated and irreversible exchange gains (i.e. exchange gains not offset by exchange loss) on new activities not part of the existing contract. Once approved in writing, the contract holder is required to submit a proposal for consideration, which should detail the funds available through exchange gains, and how these new funds will be spent across cost categories. The proposal must meet all the principles for any standard NIHR proposal especially accountability, value for money and value addition that the additional activity will bring to the wider programme of work and ODA-eligibility for ODA projects.

Mitigating against exchange rate fluctuations

Mitigating against exchange movements is the sole responsibility of the contract holder who should include this in the project design. During project implementation and as a minimum, exchange rate risks ought to be included in the contract holder’s risk register and prudently managed where there is anticipation of possible fluctuations. Unfavourable exchange rate movements may affect the project deliverables, hence the need to exercise risk-based assessment of any potential issues.

Even though the contract holder has the responsibility for exchange movements, listed below are the commonly used best practices in international development, namely:

- Proper planning and transfers: Transfers should be undertaken an appropriate number of times using the most efficient and cost-effective options

- Consideration of impact of currency conversion: It is always helpful to know the results of currency conversion and guard against preventable losses

- Transacting in stable currency: Original/contract currency is a hard currency and any currency that is stable verses original currency minimises risk.

- Reasonable sums in local currency: It is good practice to consult with downstream partners and agree reasonable sums in local currency particularly where local currency is too volatile. Contract holders are reminded that the sole responsibility for exchange variations rests with them, and they are expected to prudently manage further transfer of funds. What can be considered reasonable sums of local currency depends on planned spend, local context, acceptable minimum threshold that may be set locally, efficiency of local money/financial markets, regulatory requirements and other local factors.

- Holding funds in contract currency, GBP: This approach remains a good option. However, it is helpful to consider the functional currency used in country of operations and indeed the best location to convert the currency.

Hedging

Hedging using NIHR ODA funding is prohibited. Any occurrences of funds being used in this way will be considered a contractual breach.

Further questions on this guidance:

For further information on this guide, please email your designated Senior Programme Manager (SPM) / Programme Manager (PM) and finance department of the relevant coordinating centre (NIHR CCF Finance Team (finance&contracts@nihr-ccf.org.uk), NETSCC Finance Team (nets-finance@nihr.ac.uk) or NIHR Academy Finance Team (academy-awards@nihr.ac.uk).