Executive summary

Background

This guidance document is aimed at organisations that pay public contributors as part of their involvement in research. It is also intended for use by researchers and research staff with a responsibility for public involvement in research.

This guidance document was co-authored by staff from the National Institute for Health and Care Research (NIHR), Health Research Authority, Health and Care Research Wales, and a public contributor from Wales.

In developing this guidance document, the authors have consulted with His Majesty's Revenue and Customs (HMRC) to ensure that any references made to HMRC guidance are correct and interpretations accurate. Human Resources (HR) and finance professionals, public involvement leads, policy leads and members of the public with experience in the issue were also consulted.

The National Institute for Health and Care Research (NIHR) has developed a separate guidance document aimed at public contributors, which you might also want to view.

About this guidance document

The aim of this document is to:

- Give direction to those managing and administering payment arrangements to navigate employment status and tax regulations in an appropriate way so they feel more confident

- Provide information and links to the most appropriate HMRC guidance in order to inform decisions on payments to public contributors based on involvement activities, especially around employment status

There will be many existing public involvement roles where all parties are satisfied that there are no outstanding queries about tax and employment implications. This guidance is aimed to support individuals and organisations find common understanding for roles where there is no agreement or clear determination of employment status and/or tax.

Public contributors as individuals are responsible for their own tax affairs and ensuring that they are paying the appropriate level of tax. This guide is not intended to inform individuals of the implication of their activities on their own tax requirements, as this varies from individual to individual.

How to determine employment status - at a glance

The importance of involving people with lived experience in the research process is well understood by the research community. Accepted best practice is that public contributors are acknowledged and recognised for their time, lived experience and contribution.

Determining the employment status of public contributors helps organisations decide the most appropriate method of payment and makes clear what tax implications may arise for the organisation.

Public contributors involved in health and care research are, in most cases, not considered to be employees or casual workers. The assessment of whether public contributors are employees must be done for each involvement activity and/ or role where an assessment of employment status has not been carried out before.

To assist the decision-making process, categorisation in Chapter 2 provides illustrative examples of public contributor activities and their likely employment status and tax implications.

After having reviewed the categorisation table and made an initial assessment of likely employment status, the next step should be to review the government page describing what constitutes an employee and to decide if they are employees in HMRC’s eyes, and use the Check Employment Status for Tax (CEST) tool.

The CEST tool can be used to determine whether someone is employed or self-employed for tax and National Insurance contributions purposes. The CEST guidance pages provide useful information for completing the tool. HMRC has also recorded a webinar about the CEST tool (top of the page under ‘Webinars’).

In most cases, off-payroll working (IR35) tax does not apply to public contributors getting involved in research. Organisations can use this flowchart for client organisations (.PDF) to determine whether the organisation is affected by IR35.

A summary decision flowchart outlining the steps required to determine employment status can be found in Annex 4.

Organisations endorsing this guidance

National Institute for Health and Care Research, Health and Care Research Wales, Health Research Authority, NHS Research Scotland

Introduction

The first version of this guidance document was published in June 2022. This is the second version, which has been revised and improved incorporating feedback received.

The aim of this document is to:

- Give direction to those managing and administering payment arrangements to navigate employment status and tax regulations in an appropriate way so they feel more confident

- Provide information and links to the most appropriate HMRC guidance in order to inform decisions on payments to public contributors based on involvement activities, especially around employment status

Employment status of public contributors

Public contributors offer their independent views based on their lived experience to help inform, shape and challenge health and social care research. Whilst organisations with budgets to cover the costs of involving public contributors need to have suitable mechanisms to enable these funds to be distributed, arrangements need to reflect the status of public contributors as individuals bringing lived experience and skills to help research.

The root issue to resolve in relation to common payment challenges (as outlined in Annex 2) is determining the employment status of public contributors. The decision on the employment status of a public contributor requires consideration from the perspectives of the following:

- The individual being paid;

- The person in the organisation offering the payment in recognition of activity (usually the researcher or public involvement lead); and

- The organisation (usually the Finance Department).

The final decision on employment status should be mutually agreed by all three parties and, if needed and useful, drawing on the guidance and tools highlighted below.

There will be many existing public involvement roles where all parties are satisfied that there are no outstanding queries about tax and employment implications. This guidance is aimed to support individuals and organisations to find common understanding for roles where there is no agreement or clear determination of employment status and/or tax.

Important note - the guidance in this document is aimed at organisations or researchers/ involvement staff. Individuals are liable for their own tax and should take care to be involved in this process and seek independent advice where necessary.

How to determine employment status

Public contributors involved in health and care research are, in most cases, not considered to be employees or casual workers.

It is not possible to provide a definitive determination on employment status for all public contributors because roles and circumstances vary greatly. In fact, there may be instances where public contributors do become employees (e.g. co-applicant on a research project).

HMRC is not able to provide one single assessment for all public involvement activities. It is advised that the assessment of whether public contributors are employees must be done for each involvement activity and/ or role where an assessment of employment status has not been carried out before. This guidance document aims to delineate the steps to take to be able to make a determination on employment status.

Please note that a person may be an employee in employment law but have a different status for tax purposes.

A summary ‘decision flowchart’ outlining the steps required to determine employment status can be found in Annex 4.

Public involvement activity categorisation

To assist the decision-making process to determine employment status and tax implications, outlined below are illustrative examples of public involvement activities and their likely employment status and tax implications. Each individual role will need to be assessed on a case by case basis. It is also acknowledged that a public contributor may perform various different activities for the same organisation within a given period.

This is not intended as an exhaustive list of all types of involvement activities or public contributor roles, but is intended as a summary of the most common ones. It wouldn’t be possible to provide examples and use language which are applicable to all public involvement.

The involvement activities described below can be considered individually to be distinct, but they can also overlap. The below categories can be adapted to different contexts, research projects, organisations etc.

This categorisation is aimed at and intended to serve those involving public contributors in research, including organisations, researchers, Patient and Public Involvement leads or other professionals. For example, where it states “No obligation to deduct tax at source” it is intended from the perspective of the organisation, but the individual public contributor might need to declare payment to HMRC.

Activity example one: Attending open public meetings or events which don’t require prior preparation

For example:

- Drop-in sessions

- Open days

- Seminars

- Conferences (not presenting)

Employment status (of the public contributor):

- Not employee/ worker; unlikely to have a formal contract

Tax liability (for the organisation):

- No obligation to deduct tax at source

Activity example two: Presenting at a conference, representing an organisation/ research team and talking about the experience of being involved

Employment status (of the public contributor):

- Not employee/ worker; unlikely to have a formal contract

Tax liability (for the organisation):

- No obligation to deduct tax at source

Activity example three: Remote document review

For example:

- Funding applications

- Research materials

- Plain English summary

Employment status (of the public contributor):

- Not employee/ worker; unlikely to have a formal contract

Tax liability (for the organisation):

- No obligation to deduct tax at source

Activity example four: one-off focused and time-limited research development activities/ projects/ initiatives, typically completed within a few months. Sometimes to include preparation and remote work between meetings

For example:

- Meeting to inform research priorities

- Discuss funding applications

- Provide public perspective to research plans

- Participate in focus groups

- Help with an engagement or dissemination event

Employment status (of the public contributor):

- Not employee/ worker; unlikely to have a formal contract

Tax liability (for the organisation):

- No obligation to deduct tax at source

Activity example five: ongoing involvement in a research project or in organisational governance, providing independent advice over a period of time. Likely to include preparation and remote work between meetings

For example:

- Public contributor on research project

- Public contributor on study steering committee/ trial management group

- Public contributor on organisation steering group or governance group

Employment status (of the public contributor):

- In most cases this would not count as employment because this can be classed as providing independent advice.

Depends on:

- Length of involvement

- Level of partnership/ power sharing/ control

NOTE: Control is an important determining factor for the CEST tool (more about the CEST tool can be read below).

“The ability of a hirer to control, or have the right to control, a worker can be a strong indicator towards employment. CEST addresses the issue of control by looking at four distinct areas: control over what a worker does; control over how a worker carries out the work; control over when a worker carries out the work; control over where a worker carries out the work.”

Tax liability (for the organisation):

- Might need to deduct tax at source if employee for tax purposes

Activity example six: being a full and equal member of the research project/ organisation team, potentially carrying out research

For example:

- Public co-applicant on research project

- User-led research

- Co-researcher

Employment status (of the public contributor):

Might need contract of employment depending on:

- Person’s role within the research project

- Who controls the work

- Host institution policy

Tax liability (for the organisation):

- Tax deducted at source if employee for tax purposes

The categories were developed by the authors considering knowledge of ‘typical’ involvement activities and roles and existing payment policies and examples of where similar categories were outlined. The ‘employment status’ and ‘tax liability’ columns are informed by practical experience of relevant policies and legislation.

As outlined in Annex 2, there are several ways in which payment can be made to public contributors, including monetary and non-monetary ways. The categorisation table purposely doesn’t outline specific payment rates as there is too much variety and it is the responsibility of the organisation to determine payment rates. However, it is important to consider the total amount of payment a public contributor receives, if for example they undertake several different involvement activities for the same organisation.

After having reviewed the categorisation table and made an initial assessment of likely employment status, the next step should be to review the government page describing what constitutes an employee and to decide if they are employees in HMRC’s eyes, and use the Check Employment Status for Tax (CEST) tool. A consistent approach to assessment, action and record keeping relating to payment is key.

External professional advice to resolve any uncertainties should be sought as needed.

Check Employment Status for Tax (CEST) tool

An individual’s employment status for tax determines the taxes that need to be paid, depending on whether a worker is employed or self-employed. The CEST tool can be used to determine whether someone is employed or self-employed for tax and National Insurance contributions purposes.

The CEST guidance pages provide useful information for completing the tool. HMRC has also recorded a webinar about the CEST tool (top of the page under ‘Webinars’).

Before you start

- CEST can be used by anyone who needs to understand employment status for tax and national insurance purposes. This could include:

- The organisation hiring a worker (public contributor)

- A worker (public contributor) providing a service

- Other parties to the contract/ contractual chain

To use the CEST tool there must be a contract in place, as the tool assumes there is. A contract is an agreement (verbal or written) between a person or organisation who offers payment for something to be done for them and the person who is going to do it. The HMRC website provides more information about employment contracts and types of contracts. For example, it might be useful to know that for HMRC “an employment contract does not have to be written down.”

Before starting to use the tool, this information will be required:

- Details of the contract or agreement (which might be a verbal agreement)

- The worker’s responsibilities

- Who decides what work needs to be done

- Who decides when, where and how the work is done

- How the worker will be paid

- If the engagement includes any corporate benefits or reimbursement for expenses

In the CEST tool, a series of questions will be asked to determine employment status, on the information required as outlined above.

Once you get a CEST tool result

The tool provides the following determinations based on the information provided:

- Employed for tax purposes for this work

- Self-employed for tax purposes for this work

- Off-payroll working (IR35) rules apply (explained below)

- Off-payroll working (IR35) rules do not apply (explained below)

- ‘Unable to determine’ result; when this happens, the tool will provide further information to help reach a decision

HMRC will stand by all determinations given by the CEST tool, as long as the information given remains accurate. For this reason, it is important to keep a copy of the output for future reference.

A public contributor can also utilise the CEST tool to determine their employment status and alert the organisation that they have done so.

Where it is determined that the person is not an employee for tax purposes, then the organisation should work out if the person is a casual worker or self-employed by reviewing the government’s definition of worker, or self-employed.

HMRC’s Employment Status Manual

The HMRC internal Employment Status Manual ESM0500 is a detailed guide to determining employment status for tax. For example, it includes a section on the definition of a contract. It might also be relevant to refer to the Employment Status Manual’s page on workers for voluntary organisations.

Once an individual’s employment status has been determined, this information should help understand tax implications. The approach and principles to determine this should be discussed and agreed with the organisation’s finance and/ or HR departments/ key contacts.

Other guidance

HMRC’s Employment Income Manual (EIM71105)

The ‘HMRC 2004 Employment Income Manual (EIM71105) on Research volunteers, lay participants and participants in clinical trials guidance’ is often quoted as key guidance that has been used by organisations to determine matters pertaining to payment for public involvement. It is important to note that the HMRC Employment Income Manual as a whole is intended to serve HMRC caseworkers, and not individuals or organisations outside HMRC. However, EIM71105 remains in the public domain and as such explains HMRC’s internal approach in this area.

EIM71105 recognises:

“the use of ‘lay’ people or ‘users’ in research. Here the people in question are invited to attend meetings to give their views on various matters to inform the research process and direction. Often they will be former or current patients, representatives of particular groups such as retired people, or representatives from charities. Payment is made to them for their participation in the meetings.”

Where such circumstances exist, the guidance states that:

“HMRC agrees that the amounts paid to those concerned are unlikely to fall within the definition of ‘earnings’ for PAYE or NI purposes. No employment relationship exists and as such PAYE and NIC would be inappropriate.”

The EIM71105 also states that:

“Under Section 16, Taxes Management Act 1970, HMRC is entitled to ask for details of payments to non-employees at their discretion; but they would not routinely ask for details for small payments.”

Public involvement in research spans a variety of activities, and is not limited to participation in meetings (as explicitly referenced in the guidance). The use of the word ‘unlikely’ in the guidance means that there will be an element of interpretation involved in whether an activity falls within the direction of EIM71105. Two main factors to consider in this context are: whether involvement activities amount to employment, and whether expenses reimbursed are deemed ‘reasonable’. It is for each organisation to take responsibility to determine what they deem ‘reasonable’, and understand tax rules and apply them to their own systems and processes.

Off-payroll working (IR35) tax

This is another source of information that organisations should be aware of when determining how to pay public contributors. Off-payroll working (IR35) is the short name for the “intermediaries'' legislation. This is a set of tax rules that apply to those who work for a client through an intermediary, which can be a limited company, such as a “personal service company”. IR35 aims to stop contractors taking roles that would otherwise be paid employment but for the use of an intermediary, and to tax the engagement as if it were an employment. As public contributors are (mostly) not contractors or personal service companies, this legislation is not likely to be applicable to public involvement.

Organisations can use this flowchart to determine whether the organisation is affected by IR35. Public contributors can use this flowchart to determine if they are affected by IR35.

Implications for individuals undertaking public involvement activities

Public contributors need to be aware of any responsibility they might have in declaring income, and the organisation involving them should remind public contributors that they may need to declare involvement payment as potentially taxable income.

Public contributors as individuals are responsible for their own tax affairs and ensuring that they are paying the appropriate level of tax. This guide is not intended to inform individuals of the implication of their activities on their own tax requirements, as this varies from individual to individual.

It is recommended that the reimbursement of directly incurred (and receipted) public contributor expenses is separated from other involvement payments. Any payment that is not simply reimbursement of out of pocket expenses is potentially taxable income and whether or not an individual will have to pay tax will depend on how much other income they have. Tax for the year will only be due on a person’s income once it rises over the given personal tax allowance.

If a public contributor is self-employed, they may also have tax-free allowances for their first £1,000 of income from self-employment; the government calls this ‘trading allowance’. Public contributors should consider if this scenario may be relevant to them.

For individuals in receipt of welfare benefits, HMRC and DWP state that reimbursed expenses will not be seen as earnings and will not affect their benefits. It is best that individuals keep records of out-of-pocket expenses, e.g. a copy of a train ticket receipt. For more information on this topic please read the NIHR payment guidance.

Public contributors who receive welfare benefits

If public contributors are receiving welfare benefits, any involvement payment may affect their benefit claim. The public contributor should notify the Jobcentre Plus of any paid or voluntary activity before they do it. They may also need permission to undertake any paid activity in the first place. A service is available to provide public contributors who are in receipt of welfare benefits with free confidential advice on the impact that being paid for public involvement activities might have on their benefits. More information on this service can be found in the NIHR payment guidance.

Whilst the document co-authors recognise the importance of issues arising for public contributors who receive welfare benefits, providing detailed guidance on this topic is out of scope for this particular guidance document.

Acknowledgements

This guidance document was co-authored by staff from the National Institute for Health and Care Research (NIHR), Health Research Authority, Health and Care Research Wales, and a public contributor from Wales.

This work has been supported by a working group of public contributors, involvement staff, researchers, finance and HR staff and charity staff.

Annex 1: Background to public involvement in research

What is public involvement in research

Patient and public involvement in research is an active partnership between members of the public with lived experience and researchers in the research process. It is often described as doing research ‘with’ or ‘by’ people who use services rather than ‘to’, ‘about’ or ‘for’ them. Involvement is different from taking part in a study as a participant. Public involvement is sometimes known as ‘patient and public involvement’, ‘PPI’, or other terms.

Patients, service users and formal/ informal carers share their views, informed by what is referred to as their ‘lived experience’ of their health condition or social care situation, to inform research priorities, direction and processes. They contribute what they know is likely to be relevant, important and acceptable to the people whom the research is for or about. These insights help the professionals who plan and carry out the research ensure that their research is relevant, high-quality and impactful.

The term ‘public’ includes patients, potential patients, carers and people who use health and social care services as well as people from specific communities and from organisations that represent people who use services. Also included are people with lived experience of one or more health conditions, whether they are current patients or not. It can also include members of the public with no specific lived experience, for instance in research into disease prevention and into public health measures.

Value of public involvement

- A UK vision for The Future of UK Clinical Research Delivery was launched in March 2021. This vision aims to unleash the full potential of clinical research delivery to tackle health inequalities, bolster economic recovery and to improve the lives of people across the UK. The vision states: “Patients and service-users must also be routinely involved in the design of clinical research, to ensure outcomes match their needs and studies are designed with real participants and the realities of their daily lives in mind.”

- Funders, regulators and research organisations who play an important role in UK health and social care research came together, working with members of the public, in March 2022 to sign up to a shared commitment to improve public involvement in research.

- Public involvement can improve the quality and relevance of research. It also serves the broader democratic principles of citizenship, accountability and transparency (because most health and social care research is publicly funded).

- Meaningful public involvement is important for undertaking good, safe and ethical research and should be a routine and normal part of the research process.

- Public involvement can ensure research studies are acceptable to participate in.

- Public involvement ensures that the conduct of the study is scrutinised from a public perspective, that negative or positive results are transparently disseminated and ultimately contributes to informing improvements in care and lives.

- Diverse and inclusive involvement brings valuable diverse perspectives to research.

- Involving people in research leads to outcomes that are more relevant to people’s needs and concerns, are more robust and reliable and are more likely to be used to improve health and social care services.

Annex 2: Background to payment for public involvement in research

The importance of involving people with lived experience in the research process is understood by the research community, with funders requiring this in grant applications and demonstrated further with the development of the UK Standards for Public Involvement.

Accepted best practice is that public contributors are acknowledged and recognised for their time, lived experience and contribution. This is often in the form of monetary payment (paid through cash or bank transfer), although other reward and recognition (sometimes non-monetary) is also used by organisations, for example:

- Vouchers

- Gifts

- Access to facilities (e.g. library) or spaces

- Access to training opportunities

- Honorary appointment

Public contributors have the right to decline payment or ask for a lower amount, which might be important for individuals receiving welfare benefits. It is expected that (receipted) out-of-pocket expenses are always reimbursed. The costs of supporting public involvement in research are recognised by major research funders, who expect these to be factored into the funding arrangements from the outset and appropriately monitored via usual grant management.

Timely and flexible options to recognise contributors underpin the framework of what good public involvement should look like, as described in the UK Standards for Public Involvement. The UK Public Standards for Involvement set out clear statements of effective public involvement. The issues outlined below risk undermining organisations’ and researchers’ ability to implement these standards fully. In particular, the following could prove difficult to implement:

- Inclusive opportunities: Offer public involvement opportunities that are accessible and that reach people and groups according to research needs

- Working together: Work together in a way that values all contributions, and that builds and sustains mutually respectful and productive relationships

- Governance: Involve the public in research management, regulation, leadership and decision-making

Different levels of payment are made dependent on the types of involvement activity. In some instances, public contributors will be deemed volunteers and as such will only be offered reimbursement of expenses. This is in line with how all volunteers cross-sector are paid.

There are many types of public involvement activities, and public contributors can be involved in all stages of the research cycle. There is no ‘one size fits all’ approach to public involvement, nor indeed payment. Consequently, a flexible approach to payment is required and tailored support is needed to meet specific needs.

The expectation of research funders, government departments and health researchers is not only that public involvement is important and conducive to high-quality research, but also that more diverse communities are involved. Due to the increasing focus on health inequalities, public involvement should include involvement from groups experiencing the poorest health outcomes. Offering and facilitating payments for involvement needs to be sensitive to and take account of a diverse range of circumstances including people in receipt of welfare benefits, people on low or uncertain income, or people who may not have bank accounts.

Whilst the scope of this document is to provide organisations with practical guidance on how best to determine how people are paid, the overall intended aim is to encourage inclusivity. For example, a blanket approach to adding all public contributors to payroll could rule out people who do not have a right to work, those on benefits who are unclear on how their benefits would be impacted and those individuals without bank accounts.

A service is available to provide public contributors who are in receipt of welfare benefits with free confidential advice on the impact that being paid for public involvement activities might have on their benefits. More information on this service can be found in the NIHR payment guidance. There are increasing issues arising on the topic of the negative impact of payment on people in receipt of benefits, and further work is needed. However, this is not the current scope of this guidance document.

Payment challenges

Whilst public involvement is a routine and substantial part of the research process, researchers and professional staff across the UK consistently report ongoing challenges to ensure that recognition and reward of public contributors can be made in a suitable and efficient way. The inability to provide suitable and timely payment for public contributors undermines the ability for research to effectively involve the public, excludes certain parts of society from getting involved, wastes research funding, and causes unnecessary stress for public contributors.

Examples of common issues include:

- Confusion whether public involvement constitutes employment. This is further exacerbated by the variability of involvement activities, meaning there is no one-size-fits-all approach to address this challenge.

- There is some public sector guidance for the treatment of involvement payments that has been quoted as being referred to by organisations in the making of payment decisions. This includes for example DWP Advice for Decision Makers V4 para 4119-20, HMRC guidance EIM71100 and EIM71105 and IR35 tax information for off-payroll workers. However, feedback is that the guidance can be conflicting and can lead to confusion and inconsistencies in interpretation and application.

- There is inconsistency across the finance and HR approaches in different organisations to the treatment of involvement payments and the employment and tax status of public contributors

- Inflexible payment systems. For example, payment systems and processes are often set up for professional, corporate suppliers rather than individual members of the public

- Inconsistent payment processes, sometimes even across different parts of the same organisation.

- Where public contributors are involved in more work (e.g. they may be involved in multiple meetings and programmes within the same organisation), they will be claiming for multiple remunerable events. HR and finance departments can rightly raise queries about the employment status relating to the payments; so, this needs to be clear from the outset.

There is existing guidance available which guides and facilitates payment of involvement activities. However, the majority of confusion and problems arise when public involvement activities are assessed, and a determination of employment status and tax implications is made. This guidance document therefore specifically focuses on providing colleagues within organisations with helpful references to make assessments that result in the most appropriate payment methods and provides assurances that they are still demonstrating due diligence particularly with regards to HMRC.

In developing this guidance, the authors consulted with the HMRC to check the most appropriate guidance and correct interpretation.

Annex 3: Joint statement on the need for appropriate policies for reward and recognition of public contributors involved in health and social care research

Health and social care research provides the evidence to improve treatments, care and services for patients, service users and the public in the UK. It transforms people’s lives, promotes economic growth and advances science.

As the major funders and regulators of health and social care research in the UK, our organisations recognise the critical role of public involvement throughout the research process. Public contributors can shape research, helping to ensure research addresses questions of importance and relevance for patients, service users and the public, as well as being practical and feasible to run.

Evidence of public involvement in the design and development of research proposals, and plans for continuing public involvement in the delivery of research studies is a requirement of funding processes. It is also a key consideration in the regulatory and governance review of research studies.

Whilst public involvement approaches will vary between different research studies, the UK Standards for Public Involvement have been developed to provide a description of what good public involvement looks like and encourage approaches and behaviours that are the hallmark of good public involvement.

In line with these UK Standards, offering the appropriate payment for reward and recognition to public contributors for sharing their time, knowledge and experience is an important part of ensuring public involvement is meaningful and can draw on a diverse range of perspectives.

Our expectation is that those organisations involved in sponsoring and delivering funded research studies must have appropriate policies in place to enable flexible and timely reward and recognition payments to public contributors involved in health and social care research.

Administrative barriers to providing appropriate reward and recognition payments to public contributors are frequently referenced as one of the major challenges for undertaking meaningful public involvement in research. While these barriers persist, it undermines the ability to draw on views and contributions of the public that are representative and diverse, potentially damaging the relevance and impact of the research study. It also risks wasting research funding, where researchers are unable to utilise budgets allocated for public involvement activities.

Public involvement can include a wide spectrum of activities, and the lack of a ‘one-size fits all’ for research studies can make arrangements for providing reward and recognition complex, particularly where there may be implications on tax and employment responsibilities of organisations.

The accompanying practical guidance has been developed to support organisations to develop and implement policies that can enable appropriate reward and recognition of public contributors involvement in health and social care research, ensuring that research is ethical, relevant, high-quality and impactful.

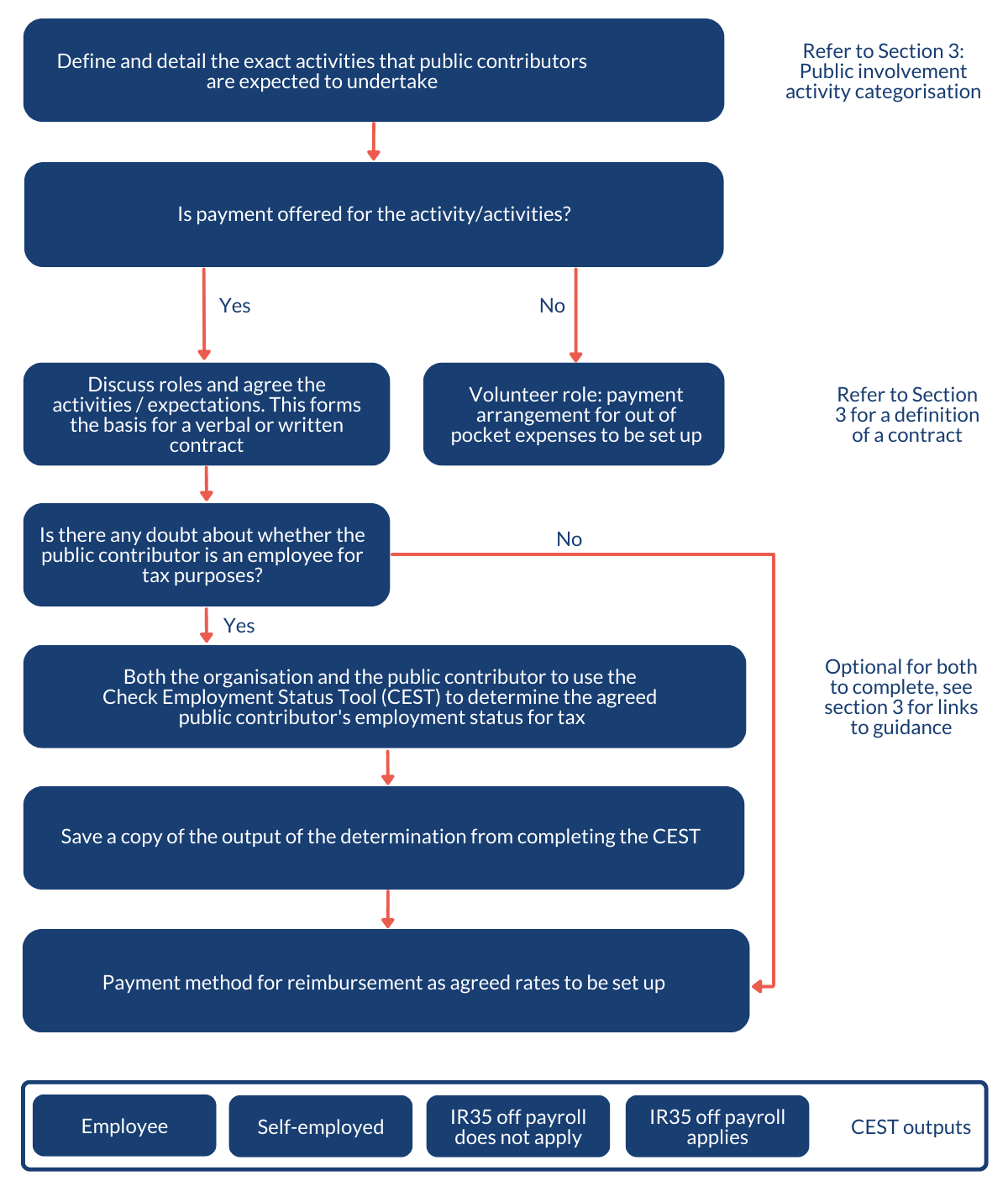

Annex 4: Decision flowchart

Accessible summary of flowchart process

- Define and detail the exact activities that public contributors are expected to undertake (refer to Section 3: Public involvement activity categorisation).

- Is payment offered for the activity/activities?

2a. If payment is offered, discuss roles and agree the activities / expectations. This forms the basis for a verbal or written contract

2b. If payment is not offered, volunteer role: payment arrangement for out of pocket expenses to be set up (refer to section 3 for a definition of a contract). - Is there any doubt about whether the public contributor is an employee for tax purposes?

3a. If yes, both the organisation and the public contributor to use the Check Employment Status Tool (CEST) to determine the agreed public contributor's employment status for tax (optional for both to complete, see section 3 for links to guidance).

3b. If no, payment method for reimbursement as agreed rates to be set up - Save a copy of the output of the determination from completing the CEST

- Payment method for reimbursement as agreed rates to be set up

CEST outputs include:

- Employee

- Self-employed

- IR35 off payroll does not apply

- IR35 off payroll applies

Annex 5: Summary of documents, links or resources

This is a compilation of all documents, links or other resources mentioned throughout the guidance document.

- UK Standards for Public Involvement

- Check Employment Status for Tax (CEST) tool

- CEST guidance pages

- Webinar about the CEST tool

- HMRC website: about employment contracts and types of contracts

- Government website: Government’s definition of worker and self-employed

- Employment Status Manual ESM0500

- Employment Income Manual (EIM71105)

- Off-payroll working (IR35)

- IR35 flowchart for organisations and for individuals

- Government website: Income Tax rates and Personal Allowances

- NIHR payment guidance for researchers and professionals

- UK vision for The Future of UK Clinical Research Delivery

- Shared commitment to public involvement

How to cite this guidance

Health and Care Research Wales, Health Research Authority and NIHR, Payment for Public Involvement in Health and Care Research: A guide for organisations on determining the most appropriate payment approach, June 2022, [URL], (Accessed on: [DATE])