Background

This guidance document is aimed at patients, carers, service users and members of the public (in this document referred to as public contributors) being offered payment as part of their involvement in health and social care research.

An Easy Read version of this guidance is also available.

The National Institute for Health and Care Research (NIHR) has also developed a separate guidance document on this subject aimed at organisations.

Introduction

What you need to know about payment for involvement

The research community understands the importance of involving people with lived experience in the research process. Funders often require public involvement in grant applications, as per the UK Standards for Public Involvement.

Best practice is that public contributors are acknowledged and recognised for their time, lived experience and contribution. This is often in the form of monetary payment (paid through cash or bank transfer), although some organisations offer other rewards and recognitions, such as:

- vouchers

- gifts

- access to facilities (such as a library) or spaces

- access to training opportunities

Monetary awards and vouchers are classed as income. As a public contributor, it is your responsibility to declare your income. The payment you receive for your involvement may be considered taxable income. Whether or not you will have to pay tax depends on how much other income you have.

You have the right to decline payment or ask for a lower amount, which might be important if you are receiving welfare benefits. It is expected that (receipted) out-of-pocket expenses are always reimbursed. Expenses are not counted as income. The costs of supporting public involvement in research are recognised by major research funders and should be factored into research budgets.

Introduction to employment status

Public contributors involved in health and care research are, in most cases, not considered to be employees or casual workers of the organisations involving them.

His Majesty’s Revenue and Customs (HMRC), the relevant government department that looks after tax and employment, is not able to provide one single employment assessment for all public involvement activities. Determining whether public contributors are employees must be done for each involvement activity and/ or role.

You should take care to be involved in the process of determining employment status where this is required and seek independent advice where necessary. Before taking part in public involvement, take care to find out your employment status, as this may affect your tax. There is more information on how to check your employment status from Citizens Advice or NI Direct.

Introduction to tax

Usually, public involvement is not classed as employment, so most organisations do not deduct tax at source for public involvement payments. Any payment that you receive that is not for reimbursement of receipted expenses is income and you may need to pay tax on it. As a public contributor you are responsible for your own tax affairs and for ensuring that you are paying the appropriate amount of tax.

What is my employment status?

It is important to note that there are many existing involvement roles where it is clear to everyone involved that there are no employment status concerns.

Where there is no agreement or clear determination of employment status, then this needs to be considered and agreed upon by:

- the individual being paid

- the person in the organisation offering the payment (usually the researcher or public involvement lead)

- the organisation (usually the Finance Department)

Often an organisation makes a decision as to whether you are employed or not in advance. However, it is important to understand how these decisions are made, and their impact before beginning an involvement activity.

We have written guidance for organisations, which contain some decision making tools that can be used to determine employment status. The following information illustrates some typical examples of involvement activities and their likely employment status:

Not likely employment

Attending open public meetings or events that don’t require prior preparation

For example:

- drop-in sessions

- open days

- seminars

- presenting at a conference, representing an organisation/ research team and talking about the experience of being involved

Document review

For example:

- funding applications

- research materials

- Patient Information Sheets

- plain English summaries

One-off and time-limited research development activities/ projects/ initiatives

Typically completed within a few months, and sometimes including preparation and remote work between meetings.

For example:

- meeting to inform research priorities

- discussing funding applications

- providing public perspective to research plans

- participating in focus groups

- helping with an engagement or dissemination event

Ongoing involvement in a research project or in organisational governance

Providing independent advice, likely including preparation and remote work between meetings.

For example:

- public contributor on a research project

- public contributor on a study steering committee/ trial management group

- public contributor on an organisation steering group or governance group

Possible employment activities

Being a full and equal member of the research project/ organisation team, potentially carrying out research

For example:

- public co-applicant on a research project

- user-led research

- co-researcher

In the companion document for organisations, several government guidelines and regulations are outlined, which can help organisations determine the employment status of public contributors. They also provide information on tax implications for the organisation. These resources can be found in Appendix 1.

What does this mean for me?

Your tax responsibilities

As a public contributor, you are responsible for declaring your income. Involvement payment could be considered taxable income.

Whether or not you will have to pay tax will depend on how much other income you have. Tax for the year will only be due on a person’s income once it rises over their given personal tax allowance.

Different payments are made for different involvement activities. In some instances, public contributors will be considered volunteers and as such will only be offered reimbursement of expenses.

Reimbursed expenses

It is recommended that organisations reimburse directly incurred (and receipted) expenses separately from other involvement payments. For example, in a payment claim form the involvement fee, travel, food and drink must be added on separate lines. Any payment for involvement that is not simply reimbursement of out-of-pocket expenses may be considered taxable income. Expenses, on the other hand, are not taxable income.

HMRC and the Department for Work and Pensions state that reimbursed expenses will not be seen as earnings and will not affect their welfare benefits. It is important that individuals keep records of out-of-pocket expenses. For example, a copy of a train ticket receipt.

If you’re self-employed

If a public contributor is self-employed, the first £1,000 earned in one year for paid activities (such as involvement) is tax-free. The government calls this ‘trading allowance’. Public contributors can check via the HMRC enquiry line or with a tax advisor if this scenario may be relevant to them.

Will my benefits be affected?

If public contributors are receiving welfare benefits, any involvement payment may affect their benefit claim. The public contributor should notify the relevant authority or office (for example Jobcentre Plus in England or the or the jobs and benefits offices in Northern Ireland) of any paid or voluntary activity before they do it. They may also need permission to undertake any paid activity in the first place.

We recognise the importance of issues arising for public contributors who receive welfare benefits, providing detailed guidance on this topic is out of scope for this document. A free and confidential advice service is available to provide public contributors who receive benefits information on how public involvement activities might impact their benefits. Ask the organisation involving you in their work if they subscribe to the Benefits Advice Service. More information on this service can be found in the NIHR payment guidance for members of the public.

Appendix 1 Government guidelines and regulations for organisations to determine employment status

The HMRC internal Employment Status Manual provides detailed information on determining employment status for tax. For example, it includes a section on voluntary work for organisations and the definition of a contract.

The ‘HMRC Employment Income Manual 71105 (on Research volunteers, lay participants and participants in clinical trials guidance)’ includes guidance which relates to involvement in research. For example, it says:

“HMRC agrees that the amounts paid to those concerned are unlikely to fall within the definition of ‘earnings’ for PAYE or [National Insurance] NI purposes. No employment relationship exists and as such PAYE and NIC would be inappropriate.”

And

“Under Section 16, Taxes Management Act 1970, HMRC is entitled to ask for details of payments to non-employees at their discretion; but they would not routinely ask for details for small payments.”

However, as we know public involvement in research spans a variety of activities and is not limited to participation in meetings (as explicitly referenced in the guidance). The use of the word ‘unlikely’ means that there will be an element of interpretation involved in whether an activity falls within the direction of The Employment Income Manual. Two main factors to consider in this context are: whether involvement activities amount to employment, and whether expenses reimbursed are deemed ‘reasonable’. It is for each organisation to take responsibility to determine what they consider ‘reasonable’ and understand tax rules and apply them to their own systems and processes.

Appendix 2: Decision flowchart

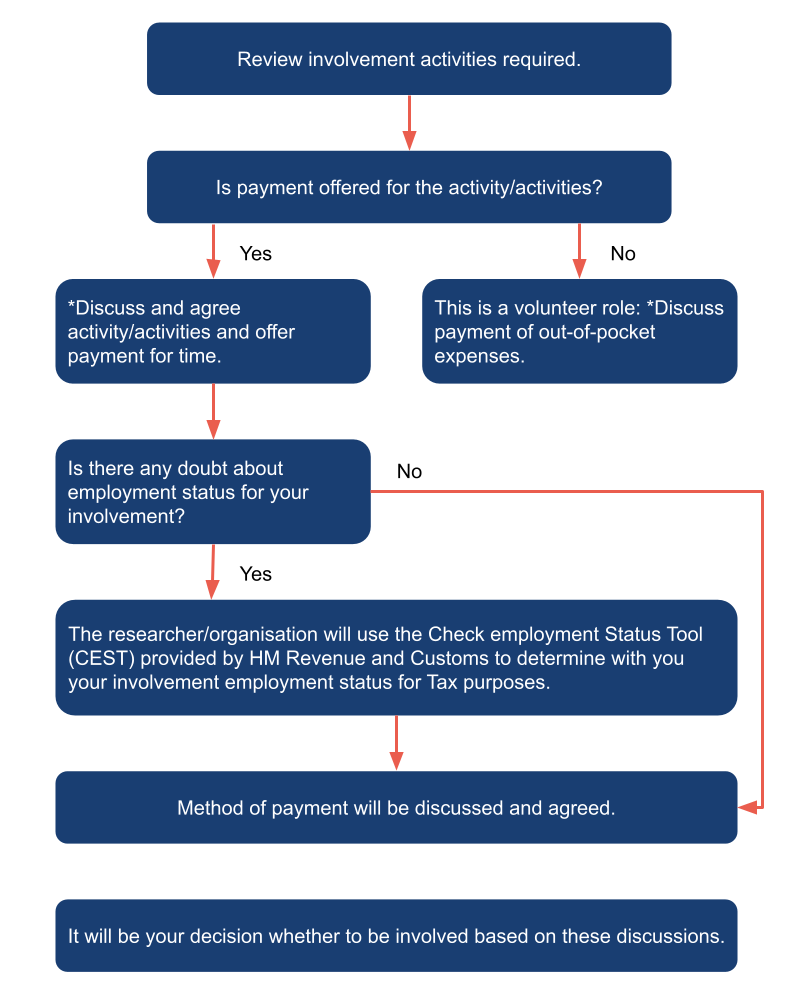

* With researcher/ organisation

Accessible summary of the flowchart process

1. Review involvement activities required.

2. Is payment offered for the activity/activities?

2a. If payment is offered: Discuss and agree activity/activities and offer payment for time (with researcher/organisation) and move to point 3.

2b. If payment is not offered, this is a volunteer role: Discuss payment of out-of-pocket expenses (with researcher/organisation).

3. Is there any doubt about employment status for your involvement?

3a. If yes, the researcher/organisation will use the Check employment Status Tool (CEST) provided by HM Revenue and Customs to determine with you your involvement employment status for Tax purposes.

4. Method of payment will be discussed and agreed.

It will be your decision whether to be involved based on these discussions.

Appendix 3: Organisations endorsing this guidance

This guidance document was co-authored by staff from the National Institute for Health and Care Research (NIHR), the Health Research Authority, Health and Care Research Wales, and a public contributor from Wales.

This work has been supported by a working group of public contributors and public involvement staff.